Commodities Update (07/07)

Over the last month the pound has been volatile against the Euro, however, it ends the period at a similar level as it started a month ago (1GBP = 1.175 EUR). Against the Dollar, the pound weakened to its lowest level since the start of Covid-19 restrictions in March 2020, however over the past 24 hours has rallied to end the day at 1GBP = 1.200 USD.

The Bank of England has hinted at further interest rate rises as it vows to bring inflation back down to 2%. In May, UK inflation hit 9.1%, its highest level in 40 years. And interest rates are at a 13-year record high of 1.25%.

The Bank of England has hinted at further interest rate rises as it vows to bring inflation back down to 2%. In May, UK inflation hit 9.1%, its highest level in 40 years. And interest rates are at a 13-year record high of 1.25%.

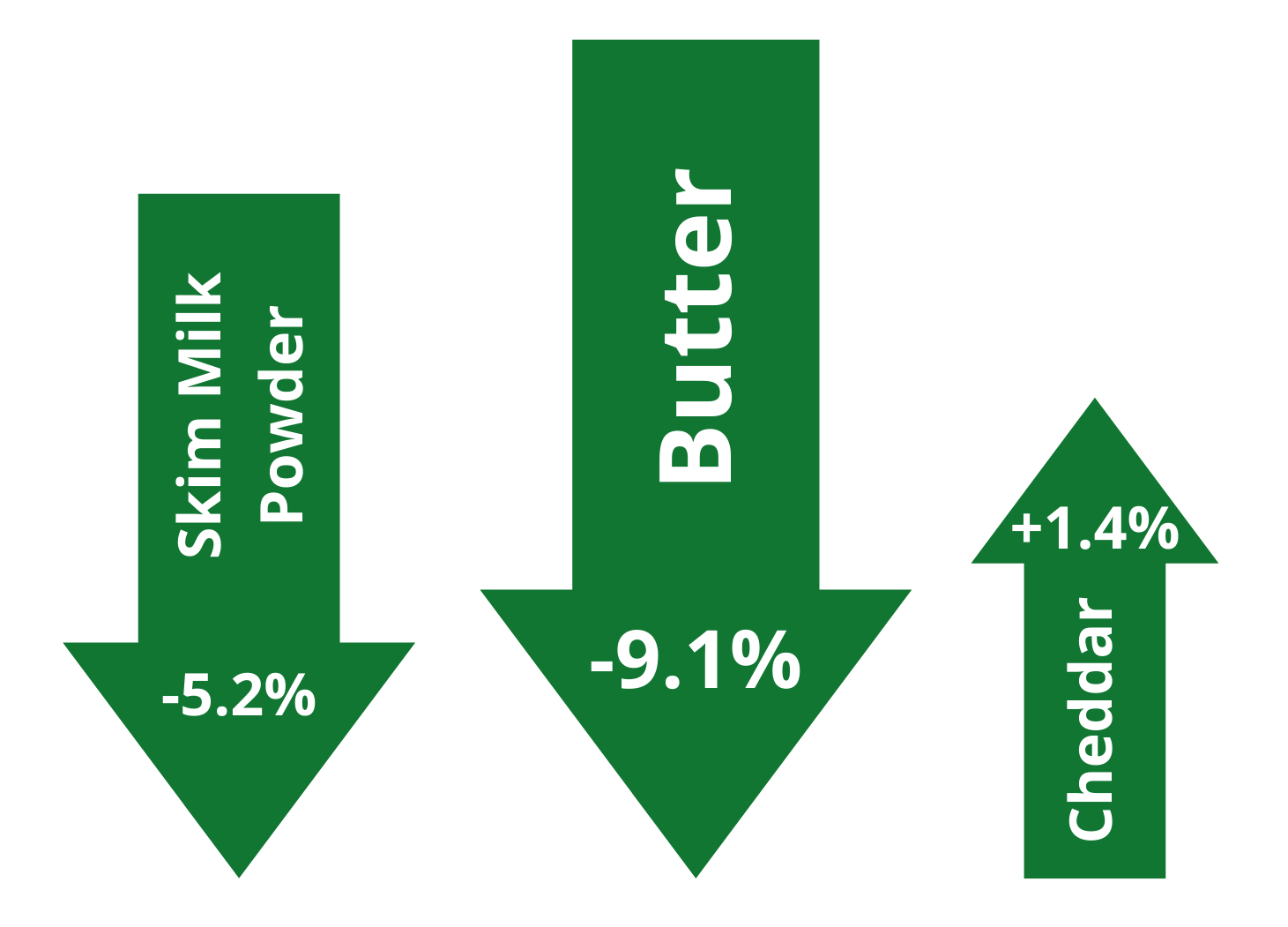

The GDT has seen significant falls of -4.1%. Notably, butter -9.1% and skim milk powder -5.2%. With a small gain for cheddar +1.4%.

Brent Crude crashed to $101.18/barrel on Tuesday (5 July), as fears of a recession mount—a scenario that could put a dent in oil demand. However, it has rallied in the last 24 hours to $104.60/barrel.

UK gas prices reached a three-month high on Tuesday (5 July) due to strikes in Norway. Current gas prices are around 290p/therm The futures price for winter 2022 is in excess of 400p/therm.

Milk Powder

Skim milk powder prices fell -5.2% at the recent GDT auction, however this will have little impact on the price of milk powder. We have seen increases of £50/tonne across a number of our milk powders this month.

Fertiliser

CF are currently withdrawn from the UK market.

Granular urea prices have risen further on global markets throughout the week, whilst the £/$ also continues to slip further. Granular Urea could see £200 to £300 increase based against £/kg of N on current ammonium nitrate prices.

European nitrate pricing remains at a premium due to continual volatility in regional gas markets and reactionary factory closures across Europe.

Potash and phosphate markets remain elevated at present. We are seeing very little interest in the potash market, with MOP values currently mid to high £700's for July delivery. However, the outlook seems firm with 40% of the supply market (Russia/Belarus) not available. Traditional nitrogen sulphur grades are also tight in supply.

Feed

Markets have continued to ease as worldwide recession and depression hit the markets, and funds settle their positions. There does appear to be a bounce this afternoon (07/07) as US markets re-assess after their holiday Monday, but general sentiment currently seems weak as we assess the harvest and future demand. Currency remains weak against the dollar keeping hipro soya at an inverse to the other markets.

For up to date prices please contact Louise on 07943 684215 or e-mail louise@dblbuyinggroup.co.uk